“Bearing” in Mind

One of the oddities of a significant bull market—and this one we’re in today qualifies, as the second-longest in modern American history—is that they tend to go on longer than you might expect from the pure market fundamentals. The last leg of a bull market tends to be driven by psychology; people have recently experienced an up market, and so they tend to expect more of the same. They buy at prices they would never consider buying at when the markets have experienced a downturn, driving prices ever higher without regard to the price. As a result, the long tail of the bull market will also see some of the greatest, fastest increases.

One of the oddities of a significant bull market—and this one we’re in today qualifies, as the second-longest in modern American history—is that they tend to go on longer than you might expect from the pure market fundamentals. The last leg of a bull market tends to be driven by psychology; people have recently experienced an up market, and so they tend to expect more of the same. They buy at prices they would never consider buying at when the markets have experienced a downturn, driving prices ever higher without regard to the price. As a result, the long tail of the bull market will also see some of the greatest, fastest increases.

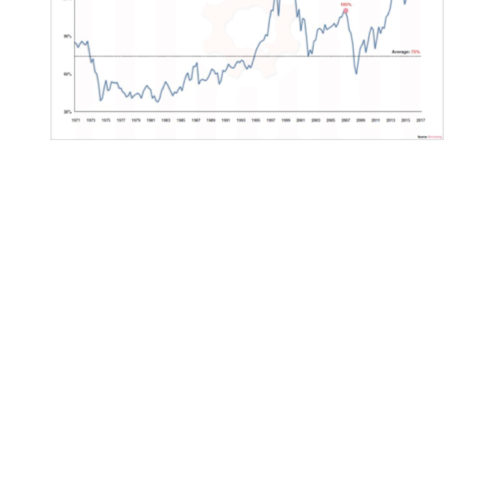

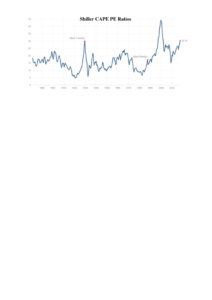

Whenever stocks become more expensive than their long-term averages, we enter a time of when a market downturn should not be a surprise. Today, as you can see from the accompanying charts, The S&P 500 index is moving into rare valuation territory. The first chart shows the evolution of the total market capitalization of the S&P 500 compared with U.S. gross domestic product. The second shows the Shiller CAPE price/earnings ratio—a popular measure of stock market valuations. In both cases, you can see that buying company earnings has actually become more expensive than it was before the Great Recession, and may be approaching the rarified territory of the dot-com bubble.

Of course, we have no way of knowing whether the next year will bring us more good news or the long-awaited downturn of 20% or more (the definition of a bear market). Other than market valuations, the signs are positive. American corporations continue to report strong earnings, economic expansion continues steadily albeit more slowly than historical norms, and a greater number of countries are experiencing sunny economic weather. Persistently low interest rates mean that investment dollars virtually have to turn to the stock market for the potential to earn reasonable returns. And, as mentioned before, the end of a bull market tends to be very generous to patient investors.

The key point to remember is that investment markets are, by their nature, volatile and unpredictable. Historically, the market has experienced a 5% correction every 7.2 months and a 10% correction every 26.1 months. We know that a more precipitous bear market (defined as a drop of 20% or more) is in our future, but we have no idea when or how. We do not practice market timing because we believe that long-term investment success comes from patience. When you jump out of the market to avoid a downturn, there is no way to make up for the returns you lost while you were on the sidelines. All we know for sure is that the next correction will represent an opportunity to rebalance and buy positions more cheaply than today’s prices—and, if the past is any indication, to sell higher down the road.

The key point to remember is that investment markets are, by their nature, volatile and unpredictable. Historically, the market has experienced a 5% correction every 7.2 months and a 10% correction every 26.1 months. We know that a more precipitous bear market (defined as a drop of 20% or more) is in our future, but we have no idea when or how. We do not practice market timing because we believe that long-term investment success comes from patience. When you jump out of the market to avoid a downturn, there is no way to make up for the returns you lost while you were on the sidelines. All we know for sure is that the next correction will represent an opportunity to rebalance and buy positions more cheaply than today’s prices—and, if the past is any indication, to sell higher down the road.

Here’s a prediction we can all be confident in: over the next few months or years, you will read financial headlines that say the bull market has a long way to run, and others that will say a devastating bear run is imminent. Please remember that nobody has a magic crystal ball. The more important thing to remember is that markets in the past have experienced terrible losses, only to experience new highs a few years later.

Post by Bob Veres

Bob Veres, a Financial Planning columnist in San Diego, is publisher of Inside Information, an information service for financial advisors.